The COVID-19 crisis has resulted in the deepest downturn in global economic activity in the post-war era, but almost certainly the shortest recession. US stocks have rebounded over 50% since the March 23rd lows and the S&P 500 is now up over 5% through three quarters. Historically, the 4th quarter is the strongest quarter of the year, but there are some potential headwinds going into year-end. The largest concerns that we are hearing from clients surround the election and what it will mean for their investments. Please click here to continue reading our 3rd Quarter Newsletter.

After the S&P 500’s worst first quarter on record, the stock market made history with an unprecedented recovery, taking many investors and prognosticators by surprise. Following the market lows reached on March 23rd, the S&P 500 was up 38% through the end of the 2nd quarter, marking one of the sharpest rallies over the past 100 years. The rally was not only monumental given the total return in just 3 months, but there was also 29 trading days (out of 70) that were up over 1%.

With assurance from Chairman Powell that “we will not run out ammunition”, along with optimism that coordinated and focused scientific research would eventually lead to a vaccine (WHO reported there are more than 100 vaccine candidates and over 20 in clinical trials), investors started to look past the pandemic and forward to an economic recovery.

We spent many hours at the end of 2019 looking at all the potential risks in the economy and markets and nowhere did we find a global pandemic caused by a bat in China. This quarter was the worst performing 1st quarter in history with the S&P 500 down 35% on March 23rd, before rallying to close the quarter down 20%. It took only 18 trading days to go from the greatest market in history to a bear market. There was no discrimination in the decline as nearly all companies suffered significant declines, regardless of their health and growth prospects. Unless we are going into a depression, we believe that much of the bad news has now been priced into stocks. However, a market bottom is typically a process and not an event. The coming months will tell us more about this recovery as the duration will dictate its shape: V, U or L.

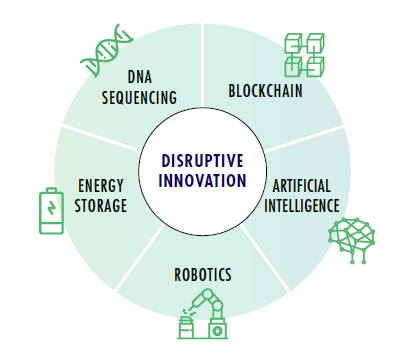

As investors continue to grapple with the near-term issues impacting global markets, we believe there is disruptive innovation happening simultaneously and could be the transformative innovation platforms that can drive the economy out of a potential recession and power growth for many years in the future. The key areas are (Source: Ark Investments):

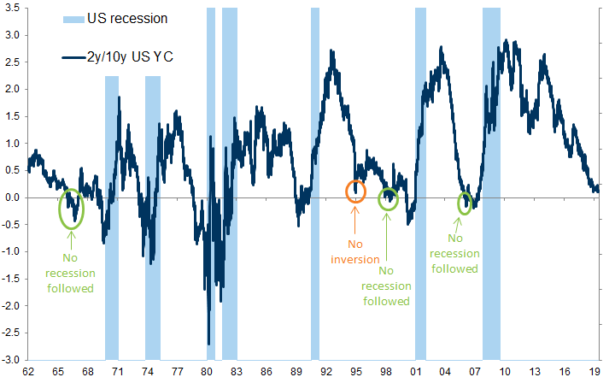

On August 14th, the 10 year Treasury Yield went slightly below the yield for the 2 year Treasury, the first time this has happened since 2007. Economist pay close attention to the 10 year vs. 2 year Treasury yields, as its historically been a strong predictor that a downturn is on the way. The yield curve has inverted before every US recession since 1955, although it sometimes happens months or years before the recession starts. The average time between the last 5 yield curve inversions and a recession was 17 months. This lead time is the key and its still very uncertain how long a lead time we may have in the current economy before there is an actual recession. That said, an inverted yield curve, like most other indicators, is not perfect and doesn’t mean a recession is imminent.