“No Man’s life, liberty, or property are safe while the legislature is in session” -Mark Twain

Over the past week, Neil and I have received many questions about the government shutdown and impending debt ceiling and how they might affect the markets. So we thought we would share with you a quick summary of what we believe is happening and how we are positioning our portfolios as a result.

We at Canal Capital Management are big believers in ETFs, otherwise known as Exchange Traded Funds, because of their salient characteristics: cheap, tax efficient, intra-day trading, index replicating, etc., But just like with any investment product, they are not all created equal. Due diligence is required when investing in any ETF. At our firm, we follow a disciplined process when vetting any investment, and ETFs are no exception. We apply the following test: Efficiency, Tradability & Fit. Efficiency looks at a fund’s costs, while Tradability assesses average daily trading volume, and Fit examines the securities the fund owns. Though it may sound corny, this mnemonic device describes a process by which we narrow down some 1,500 ETFs to a more manageable security universe of choices that will best fit our investment objectives.

Over the past week, I have had several clients mention the recent PBS Frontline special, “The Retirement Gamble” (Retirement Gamble). I have also read several negative comments from my industry regarding the piece. After finally finding the time to watch it this morning, I believe it was honest and well done. It is refreshing to see PBS do a piece that includes two of the three messages we try to relay to investors every day.

A Fiduciary places investors interest before their own

Fees steal returns and are one of the most important determinants in investment outcomes

by Neil Gilliss, MBA, CFP | Mar 19, 2013 | Investments

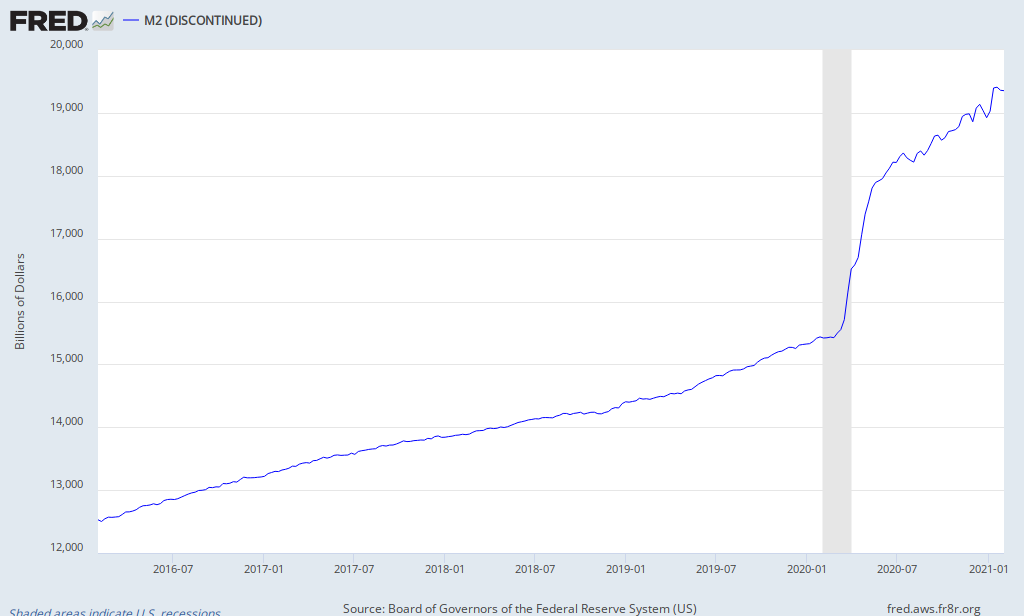

The general idea about inflation we are taught is that the greater the supply of money, the less a single dollar is worth, and the prices for the goods we buy should rise. This simple model usually holds true, yet policies by the Federal Reserve over the past five years have substantially increased the supply of money but have failed to stimulate above average inflation. Inflation lowers everyone’s purchasing power and erodes the real return on investments, so keeping an eye on when inflation might rise is important.

People have long viewed bonds as a relatively risk free asset class, and who could blame them; since 1983, the Barclays Aggregate Bond Index has had an 8.1% average annual compound rate of return. During that period, it suffered only 3 negative years, with -2.9% being its worst. With interest rates inevitably rising, these numbers cannot continue. Bonds will switch from being risk free to risky. This “great rotation” from Bonds to Stocks will not be done without angst. Investors’ perception of risk will have change and managers who made their careers during the bond bull market will evolve while a new era of asset allocation is ushered in.